http://www.theaustralian.com.au/national-affairs/bank-bashers-risk-economy-say-leaders/comments-fn59niix-1226256750657

PROFITABLE and well-funded banks are critical to the health of the Australian economy at a time of global uncertainty, bank leaders warned as they urged politicians to stop bashing the big four financial institutions.

- The Australian, 30th Jan 2012.

I really wonder what the intent of running such a thing on the front page of the Oz is. Presumably it's either the banks trying to use media pressure to make the government change policy or it's just the Oz trying to curry favour with its potential advertising base. Whatever the case, I think that the article almost hints at economically illiteracy.

To wit:

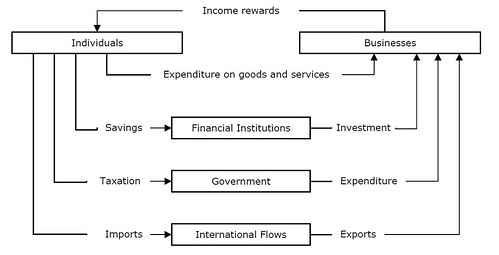

In and Economics 101 class on the very first day we would have seen this diagram:

The most basic two sectors of the economy are the Households and Firms. Whilst it's handy to note where the money is flowing in the form of wages and spending, it's even more fundamental to note what ultimately drives every single transaction which exists and which has driven every single economy since before time dot.

Every economy has at its base, the production of goods and services. Heck, we even measure the overall health of the economy on this measure with GDP. The figure of GDP or Gross Domestic Product, is the final market value of all goods and services produced within a country within a financial year.

Whilst it might be true that the banking sector does help to enable the transfer of funds which can be made available for investment, the biggest drivers of GDP are things which are actually being produced and services which are genuinely being performed.

If we take the current Australian economy as an example, the state currently experiencing the greatest growth is Western Australia. Why? Because Western Australia currently is producing a lot of raw goods. Of course it would make logical sense if the Australian economy itself would produce more elaborately transformed goods but we don't seem to be able to do so.

Historically the world's biggest powers have also risen to power on the basis of goods being made and services being performed. In the ancient world, a nation grew more powerful with more people under its control. Admittedly in a world in which agriculture was the biggest single sector, then this was very closely linked to the area of land which a nation could control.

During the Industrial Revolution and the rise of Entrepreneurs, the focus shifted from agricultural products to other sorts of products. We can basically follow the rise of nations with the sorts of products they produced, Britain, the United States and now China have all risen (and sometimes fallen) on the basis that they could make stuff and sell it.

The thing is that the banking sector whilst providing the service of buying and selling funds, is entirely funded on the basis of other sectors in the economy producing goods and services.

I take issue with the statement "PROFITABLE and well-funded banks are critical to the health of the Australian economy" for two rather glaringly obvious reasons.

1. The truth is that if there were no domestic banks at all in Australia, the economy would still function more or less perfectly. The process of producing goods and services would continue as it has done for centuries. In fact the whole idea of banking in a modern context didn't even start until the renaissance. The word bank itself comes from the Old Italian "banca" which described the tables or benches upon which the businesses of houses like Medici, Peruzzi and Bardi operated.

Even in a modern context, a bank is little more than a coupon shifter. Profits are extracted from "customers" who borrow money from the bank and then have to pay back the principle plus interest and the extra money which is used to pay interest comes from the production of goods and services.

2. The implication of the phrase "PROFITABLE and well-funded banks" suggests that Australia has banks which are not profitable or well funded. Just to put this in perspective, the profits as listed in 2011 by just the big four banks were as follows: NAB $5.220bn, WBC $6.991bn, CBA $4.723bn, ANZ $4.510bn. Together they made $21,444,000,000 in profit. The suggestion that the banks in Australia are not profitable is both idiotic and/or an outright lie (mind you, given the rest of News Corp's abilities to make up news, it's not beyond the Australian to lie on it's front cover).

Also, the big four banks have collectively $3,276,512,000,000 in funds under management. Perhaps the Australian would like to explain just how it is that just four banks with more than three trillion dollars under management are some how not "well-funded".

There was one line in the article which I gagged at, which was:

"The Reserve Bank could move on rates as soon as next week because of job layoffs and poor consumer and business confidence, "

Job layoffs? Perhaps we should point the finger at the banks themselves on this one:

http://www.theaustralian.com.au/business/companies/westpac-forecasts-job-cuts-suncorp-sends-back-office-work-to-india/story-fn91v9q3-1226253683491

AUSTRALIA'S financial services industry delivered another blow to the country's workforce today with news of pending job losses and work functions heading offshore.

Suncorp Group said it will cut 71 jobs at its insurance arm to improve back-office efficiency and Westpac said it expects to finish the financial year with fewer staff, the companies said today.

The job cuts are the latest to hit workers in Australia's financial services sector, after ANZ Banking Group announced plans to cut about 130 jobs last week; investment bank UBS predicted that Australia's banks will shed 7000 jobs in the next two years.

-The Australian, 25th Jan 2012.

Poor consumer and business confidence? Well, considering that the Global Financial Crisis itself was caused by the banking sector and their predatory lending practices; allowing ridiculously easy credit to people who should have never been allowed to borrow in the first place which led to a hideous undervalue in the pricing of risk and even dare I suggest outright fraudulent underwriting practices, then wouldn't those things lead to poor consumer and business confidence?

No, the reason for running such an article is to do with Don Argus the former NAB CEO and current NAB chairman Michael Chaney probably have a "quiet talk" with the Australian's editor-in-chief Chris Mitchell. Mind you, Mitchell himself isn't averse to lying either. I guess any excuse to bash the government is good enough, even if you have to write a great big pile of balderdash, blather and bunkum.

No comments:

Post a Comment